Jim Cramer and Elon Musk Both Criticized Social Security, but Retirees Need the Full Story

Millions of retirees depend on Social Security as a major source of income, and millions of current workers are counting on those benefits to be there when they leave the workforce. That is why comments from high-profile figures like Jim Cramer and Elon Musk can get so much attention. Both have compared Social Security to a Ponzi scheme, with Musk making that claim publicly in 2025, but that framing leaves out important context. Social Security is a legal federal insurance program funded mainly through payroll taxes, not an illegal investment fraud. Fact-checkers have noted that while the program does use current worker contributions to help pay current beneficiaries, it is transparent, government-run, and subject to oversight in ways a Ponzi scheme is not.

That does not mean Social Security is financially problem-free. The program faces long-term funding pressure as the population ages, birth rates shift, and fewer workers support each beneficiary compared with earlier generations. For retirees and future retirees, the real takeaway is not that Social Security is a “scam,” but that it may not be enough to rely on by itself. This My Investing News piece looks at why Cramer and Musk have criticized the system, what they get right and wrong, and what Americans should understand about Social Security before building a retirement plan around it.

Jim Cramer and Elon Musk Called Social Security a Ponzi Scheme

Jim Cramer and Elon Musk have both compared Social Security to a Ponzi scheme, and Musk has gone even further by calling it the biggest Ponzi scheme of all time. That kind of claim gets attention because millions of retirees depend on Social Security, and millions of workers are counting on it for future income. But the comparison leaves out a lot. Social Security has financial problems that retirees should understand, but that does not make it a scam. The real issue is whether the program can keep paying full scheduled benefits without changes from Congress.

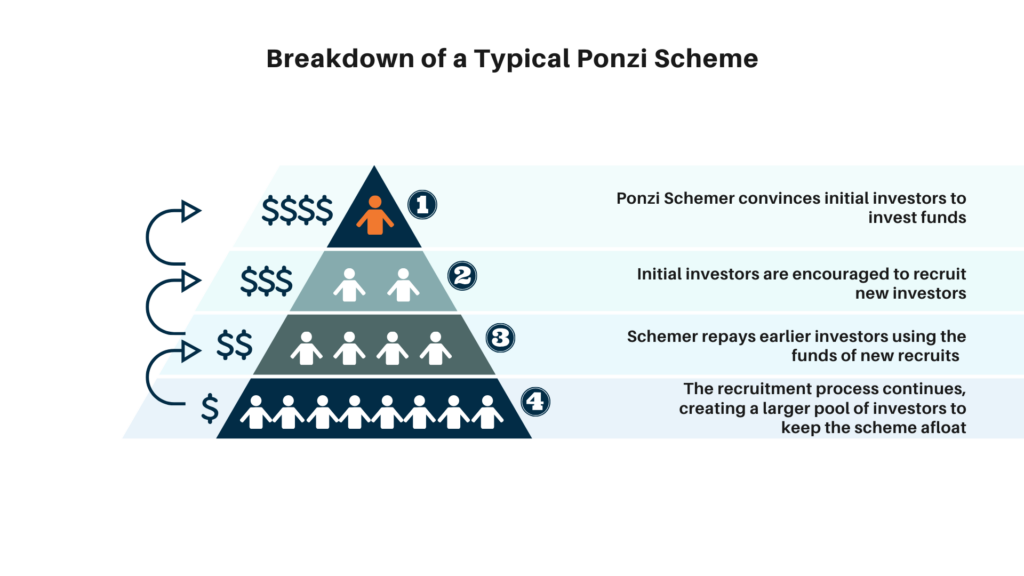

What a Ponzi Scheme Actually Is

A Ponzi scheme is a form of investment fraud. In a typical Ponzi scheme, early investors are paid with money collected from newer investors, while the organizer creates the false impression that those payments are coming from legitimate profits. The scheme depends on deception, unrealistic promises, and a steady flow of new money. When enough new investors stop coming in, the fraud collapses. That is very different from a public benefit program that is created by law, funded through taxes, and required to report its finances openly.

Why Social Security Does Not Fit That Definition

Social Security is not an illegal investment operation. It is a federal insurance program that pays retirement, disability, survivor, and family benefits to eligible Americans. Workers and employers pay into the system through payroll taxes, and those revenues help fund benefits for current beneficiaries. The program does not secretly promise impossible investment returns, and its finances are reviewed and published each year by the Social Security Trustees. That transparency is one of the biggest reasons the Ponzi scheme label does not fit, even if critics dislike the program’s pay-as-you-go structure.

The Program Still Has a Real Funding Problem

Calling Social Security a scam is inaccurate, but pretending the program is financially fine would be wrong too. The 2025 Trustees Report projects that the combined retirement, survivors, and disability trust funds can pay full scheduled benefits until 2034. After that, if Congress does nothing, incoming revenue would be enough to cover only about 81% of scheduled benefits. That does not mean checks disappear, but it does mean future retirees could face smaller payments than they were promised unless lawmakers raise revenue, reduce benefits, or make some combination of changes.

The Shortfall Is About Demographics, Not Theft

Social Security’s pressure comes largely from demographics. The program relies heavily on payroll taxes from current workers, but the population is aging, people are living longer, and the ratio of workers to beneficiaries is not as strong as it once was. As more older Americans leave the workforce and claim benefits, the program has to pay out more while relying on a smaller base of workers per retiree. That is a serious math problem, but it is not the same thing as government officials stealing payroll taxes or secretly running a fraud.

Social Security Was Never Meant to Be Your Whole Retirement Plan

Even if Congress prevents benefit cuts, Social Security is not designed to replace a full paycheck. The Social Security Administration says benefits replace only a percentage of pre-retirement income, and the exact amount depends on a worker’s earnings history and claiming age. For many average earners, the replacement rate is often discussed around 40%, which leaves a large gap for housing, food, health care, taxes, insurance, and everyday expenses. That makes Social Security an important foundation, but not a complete retirement plan.

Retirees Need Income Outside Social Security

The safest takeaway is not that Social Security is a Ponzi scheme. It is that relying on Social Security alone can leave retirees exposed. A stronger retirement plan may include a 401(k), IRA, taxable brokerage account, pension income, annuity income, rental property, cash savings, or part-time work. Not every household will use the same mix, and not every option is realistic for every retiree. But having even one or two additional income sources can reduce the risk that a benefit cut, inflation spike, or medical bill upends a retirement budget.

The Bottom Line for Future Retirees

Cramer and Musk are right to draw attention to Social Security’s long-term financial strain, but the Ponzi scheme label oversimplifies the issue and makes the problem sound more fraudulent than it is. Social Security is a legitimate federal program with public financing and public reporting. The concern is that the program may not be able to pay full scheduled benefits without reform. For retirees and workers, the smart move is to treat Social Security as one part of a larger plan, not the only paycheck they expect to have in retirement.